“I’ve had many discussions with Yves and followed his trajectory over the past few years. He is basically a full time professor with a side job as a leading expert in Python for quantitative finance who travels around the world consulting WS and educationally paving the way for any kid who dreams of not just being a Quant, but a new, cutting-edge type of one. For myself having spent most of my career in volatility, he is an invaluable resource. Be warned though this is the third book in his Python quant collection and for most people they’ll be better off starting with his first two works.”

“Volatility derivatives are a class of derivative securities where the payoff explicitly depends on some measure of the volatility of an underlying asset. Prominent examples of these derivatives include variance swaps and VIX futures and options” Peter Carr and Roger Lee (2009) — Volatility Derivatives, Annual Review of Financial Economics.

ORDER HERE

About the author

Dr. Yves J. Hilpisch is founder and CEO of The Python Quants (https://tpq.io) and The AI Machine (https://aimachine.io). The group focuses on Open Source technologies for Financial Data Science, Artificial Intelligence, Algorithmic Trading, Computational Finance, and Asset Management. It also provides data, financial and derivatives analytics software (see Quant Platform and DX Analytics) as well as consulting services and Python for Finance online and corporate training programs.

Furthermore, Yves organizes Python for Finance, AI, and Algorithmic Trading Meetup group events in Berlin, Frankfurt, Paris, London (see Python for Quant Finance) and New York (see AI & Algo Trading).

Quant Platform

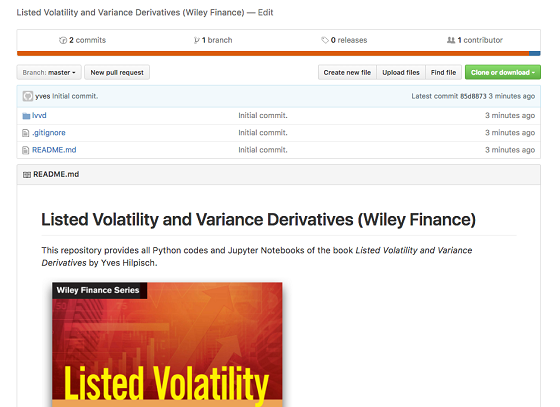

All Python codes (scripts, modules, etc.) as well as complementary Jupyter Notebooks for immediate execution will be made available on the Quant Platform. No installation necessary, just an easy and quick registration necessary under

All Jupyter Notebooks and all Python code files for easy cloning and local usage are available on Github. Make sure to have a comprehensive scientific Python installation (2.7.x) ready.

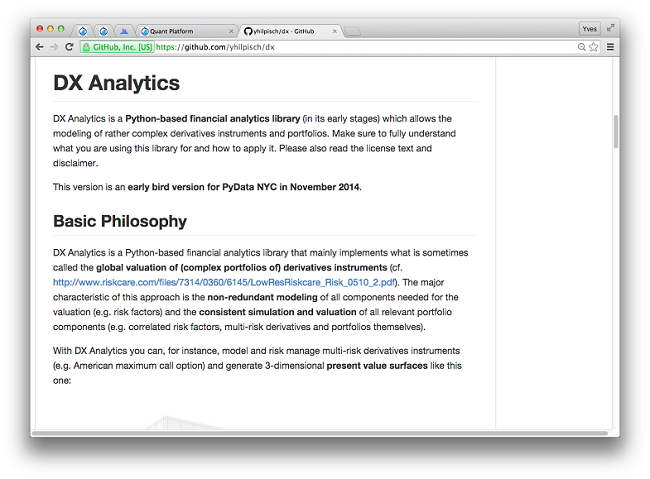

DX Analytics is a purely Python-based derivatives and risk analytics library which implements all models and approaches presented in the book (e.g. stochastic volatility & jump-diffusion models, Fourier-based option pricing, least-squares Monte Carlo simulation, numerical Greeks) on the basis of a unified API.

We are offering comprehensive Python for Finance online training programs — leading to University Certificates — about Financial Data Science, Algorithmic Trading, Computational Finance, and Asset Management. In addition, we also offer customized corporate training classes. See https://certificate.tpq.io or just get in touch below.

Get & Keep in Touch

DR YVES J HILPISCH

Write me under lvvd@tpq.io. Stay informed about the latest in Open Source for Quant Finance by signing up below.

The Experts in Data-Driven and AI-First Finance with Python. We focus on Python and Open Source Technologies for Financial Data Science, Artificial Intelligence, Algorithmic Trading and Computational Finance.